Valuation with Existing Shareholder TPG Capital to Reinvest via TPG Asia Fund, Founded in 1997 by Alek Safarian Who Stepped Down as CEO in 2025 March")

& National Rally Party Convicted of €3 Million ($3.3 Million) Embezzlement with Marine Le Pe Sentenced to 4-Year Jail Term (2 Suspended + 2 Electronic Tag), €100,000 Fine & 5-Year Public Office Ban by France Court, Marine Le Pen & National Rally Party Diverted €3 Million from European Union (EU) Funds to Pay France Staff")

to Sell 33% of UBS Securities in China, UBS Currently Owns 67% of UBS Securities in China")

Succeeding Tan Sri Abdul Wahid Omar Who is Retiring (30/4/25) after 5-Year Tenure as Chairman, Tan Sri Abdul Farid Alias Has 30 Years of Financial Services & Banking Experience Including at Maybank, JP Morgan, Malaysian International Merchant Bankers & Schroders")

Assets under Trust in 2023, 4 Key Sectors are Corporate Trusts, Pension Schemes, Private Trusts & Charitable Trusts, Assets by Client Type are Public Funds 30%, Pension Funds 38% & Others 30%, Introduction of Type 13 Regulated Activity (RA 13) in 2024 October to Regulate Corporate Trustees & Depositaries and to Increase Trust Industry Credibility, HKMA Supervisory Policy Manual Module TB-1 (SPM TB-1) Launched to Protect Client Assets & Promote Fair Treatment of Clients, 6,783 Trust / Company Service Provider (TCSP) Licensees as of 2024 November (331 Trust Service, 1,978 Trust & Company Service, 4,474 Company Service), Top 5 Expected Growth Engines in Trust Industry are China Mainland & GBA, Virtual Assets, Capital Investment Entrant Scheme (CIES), Family Office & Philanthropy, ESG Funds")

The 2025 Investment Day | 2025 Family Office Summits | Family Office Circle

Investment / Alternatives Summit - March / Oct / Nov

Investment Day - March / July / Sept / Oct / Nov

Private Wealth Summit - April / Oct / Nov

Family Office Summit - April / Oct / Nov

View Events | Register

This site is for accredited investors, professional investors, investment managers and financial professionals only. You should have assets around $3 million to $300 million or managing $20 million to $30 billion.

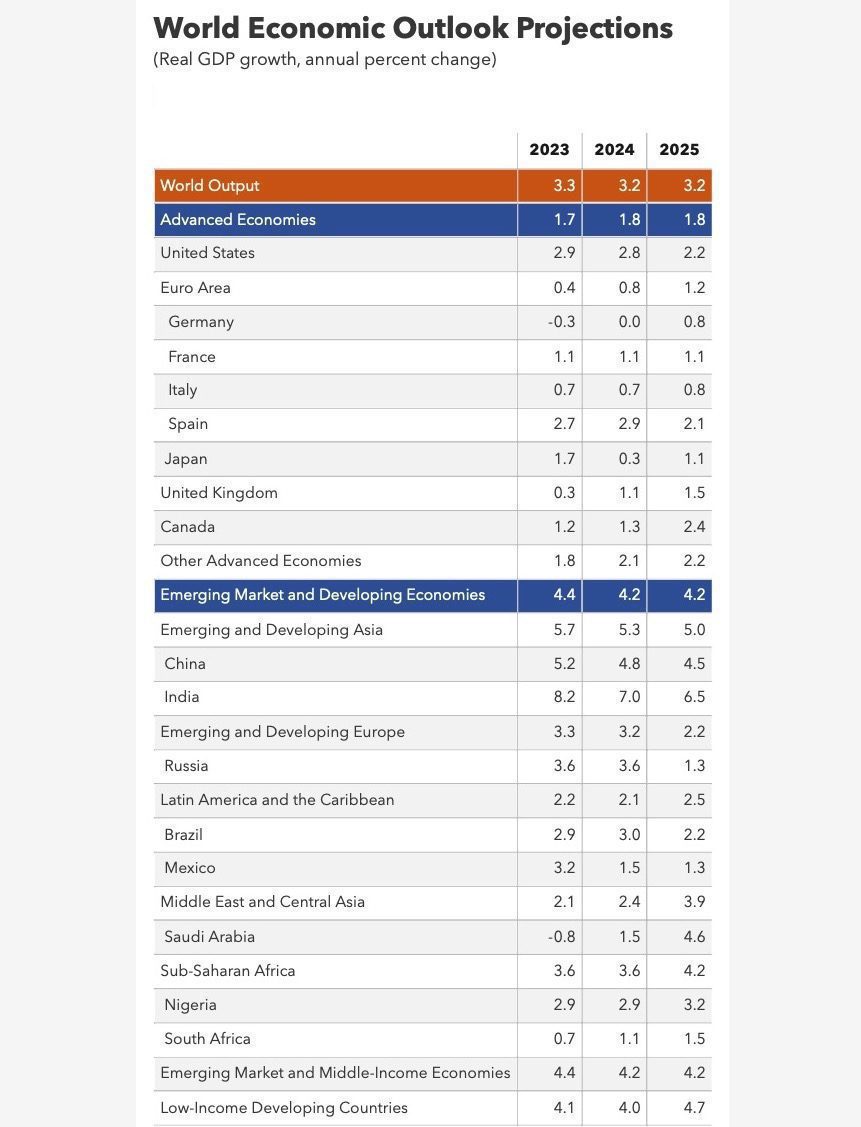

IMF World Economic Outlook 2024: Global GDP to Grow +3.2% with +5.8% Inflation in 2024, United States +2.8% & China +4.8% in 2024, 2 Growth Upside – Stronger Recovery in Investment in Advanced Economies & Stronger Momentum of Structural Reforms, 7 Downside Risks – Monetary Tightening, Financial Markets Reprice Due to Monetary Policy, Sovereign Debt Stress in Emerging & Developing Economies, China Property Sector Contracts More Deeply, Renewed Spikes in Commodity Prices Due to Climate Shocks, Regional Conflicts or Geopolitical Tensions, Protectionist Policies & Social Unrest

1st November 2024 | Hong Kong

The International Monetary Fund (IMF) has released the IMF World Economic Outlook 2024 (October Update), providing key insights into global economy & GDP growth in 2024 & 2025. Global GDP is expected to grow +3.2% in 2024 and +3.2% in 2025, with global inflation forecast at +5.8% in 2024 and +4.3% in 2025 (2023: +6.7%). United States GDP growth forecast in 2024 / 2025 +2.8% / +2.2% and China +4.8% / +4.5%. 2 Growth Upside – Stronger recovery in investment in advanced economies, Stronger momentum of structural reforms. 7 Downside Risks – Monetary policy tightening, Financial markets reprice as a result of monetary policy reassessments, Sovereign debt stress intensifies in emerging market and developing economies, China’s property sector contracts more deeply than expected, Renewed spikes in commodity prices arise as a result of climate shocks, regional conflicts, or broader geopolitical tensions, Countries ratchet up protectionist policies, Social unrest resumes. Central Bank policies recommendations / priorities – Managing the final descent of inflation, Rebuilding buffers to prepare for future shocks and achieving debt sustainability, Enabling durable medium-term growth, Strengthening resilience through multilateral cooperation. 2024 Global Outlook – Global battle against inflation has largely been won. Inflation peaked at 9.4% YOY in Q3 2022, projected to reach 3.5% by the end of 2025, below average level of 3.6% between 2000 and 2019. Global economy unusually resilient throughout the disinflationary process, avoiding a global recession. Downside risks are rising and now dominate the outlook: an escalation in regional conflicts, monetary policy remaining tight for too long, a possible resurgence of financial market volatility with adverse effects on sovereign debt markets, a deeper growth slowdown in China, and the continued ratcheting up of protectionist policies. World dominated by supply disruptions – from climate, health, and geopolitics. Harder for monetary policy to maintain price stability when faced with such shocks, which simultaneously increase prices and reduce output. Level of uncertainty surrounding the outlook is high – Newly elected governments (about half of the world population has gone or will go to the polls in 2024) could introduce significant shifts in trade and fiscal policy. Little change in the global growth outlook since the April 2024 World Economic Outlook. Following the post-pandemic rebound, the global projection for GDP growth has been hovering at about 3%, both in the short and the medium term. See below for key findings & summary | View report here

“ IMF World Economic Outlook 2024: Global GDP to Grow +3.2% with +5.8% Inflation in 2024, United States +2.8% & China +4.8% in 2024, 2 Growth Upside – Stronger Recovery in Investment in Advanced Economies & Stronger Momentum of Structural Reforms, 7 Downside Risks – Monetary Tightening, Financial Markets Reprice Due to Monetary Policy, Sovereign Debt Stress in Emerging & Developing Economies, China Property Sector Contracts More Deeply, Renewed Spikes in Commodity Prices Due to Climate Shocks, Regional Conflicts or Geopolitical Tensions, Protectionist Policies & Social Unrest “

Caproasia Access | Events | Summits | Register Events | The Financial Centre

The 2025 Investment Day | 2025 Family Office Summits | Family Office Circle

Basic Member: $5 Monthly | $60 Yearly

Newsletter Daily 2 pm (Promo): $20 Monthly | $180 Yearly (FP: $680)

Hong Kong | Singapore

March / July / Sept / Oct / Nov

Private Equity, Hedge Funds, Boutique Funds, Private Markets & more. Join 20+ CIOs & Senior investment team, with > 60% single family offices with $300 million AUM. Taking place in Hong Kong and in Singapore. Every March, July, Sept, Oct & Nov.

Visit | Register here

10th April & 16th Oct Hong Kong Ritz Carlton | 24th April & 6th Nov Singapore Amara Sanctuary Resort

Join 80 single family offices & family office professionals in Hong Kong & Singapore

Links: 2025 Family Office Summit | Register here

March / Oct / Nov in Hong Kong & Singapore

Join leading asset managers, hedge funds, boutique funds, private equity, venture capital & real estate firms in Hong Kong, Singapore & Asia-Pacific at the Investment / Alternatives Summit. Join as delegate, speaker, presenter, partner & sponsor.

Visit | Register here

April / Oct / Nov in Hong Kong & Singapore

Join CEOs, CIOs, Head of Private Banking, Head of Family Offices & Product Heads at The Private Wealth Summit. Join as delegate, speaker, presenter, partner & sponsor.

Visit | Register here

IMF World Economic Outlook 2024: Global GDP to Grow +3.2% with +5.8% Inflation in 2024, United States +2.8% & China +4.8% in 2024, 2 Growth Upside – Stronger Recovery in Investment in Advanced Economies & Stronger Momentum of Structural Reforms, 7 Downside Risks – Monetary Tightening, Financial Markets Reprice Due to Monetary Policy, Sovereign Debt Stress in Emerging & Developing Economies, China Property Sector Contracts More Deeply, Renewed Spikes in Commodity Prices Due to Climate Shocks, Regional Conflicts or Geopolitical Tensions, Protectionist Policies & Social Unrest

The International Monetary Fund (IMF) has released the IMF World Economic Outlook 2024 (October Update), providing key insights into global economy & GDP growth in 2024 & 2025. See below for key findings & summary | View report here

IMF World Economic Outlook 2024

GDP Growth Forecast (2024 / 2025):

- Global: +3.2% / +3.2%

- Advanced Economies: +1.8% / +1.8%

- Emerging Market and Developing Economies: +4.2% / +4.2%

Global Inflation Forecast (2024 / 2025): +5.8% / +4.3% (2023: 6.7%)

2024 / 2025 GDP Growth forecast in Americas:

- United States: +2.8% / +2.2%

- Canada: +1.4 / +2.3%

- Brazil: +1.3% / +2.4%

- Mexico: +1.5% / +1.3%

2024 / 2025 GDP Growth forecast in Europe:

- United Kingdom: +1.1% / +1.5%

- Germany: 0% / 0.8%

- France: +1.1% / +1.1%

- Italy: +0.7% / +0.8%

- Spain: +2.9% / +2.1%

- Netherlands: +0.6% / +1.6%

- Switzerland: +1.3% / +1.3%

- Russia: +3.6% / +1.3%

2024 / 2025 GDP Growth Forecast in APAC:

- China: +4.8% / +4.5%

- India: +7% / +6.5%

- Japan: +0.3% / +1.1%

- South Korea: +2.5% / +2.2%

- Taiwan: +3.7% / +2.7%

- Hong Kong: +3.2% / +3%

- Singapore: +2.6% / +2.5%

- Indonesia: +5% / +5.1%

- Malaysia: +4.8% / +4.4%

- Thailand: +2.8% / +3%

- Philippines: +5.8% / +6.1%

- Vietnam: +6.1% / +6.1%

- Australia: +1.2% / +2.1%

- New Zealand: 0% / +1.9%

2024 / 2025 GDP Growth Forecast in Middle East:

- UAE: +4% / +5.1%

- Saudi Arabia: +1.5% / +4.6%

Top 10 Economies in the World (GDP):

- United States – $27.3 trillion

- China – $17.7 trillion

- Germany – $4.4 trillion

- Japan – $4.2 trillion

- India – $3.5 trillion

- United Kingdom – $3.3 trillion

- France – $3 trillion

- Brazil – $2.2 trilion

- Italy – $2.2 trillion

- Canada – $2.1 trillion

Top 15 Economies in Asia-Pacific (GDP):

- China – $17.7 trillion

- Japan – $4.2 trillion

- India – $3.5 trillion

- South Korea – $1.7 trillion

- Australia – $1.7 trillion

- Indonesia – $1.3 trillion

- Taiwan – $755 billion

- Thailand – $514 billion

- Singapore – $501 billion

- Bangladesh – $437 billion

- Philippines – $437 billion

- Vietnam – $433 billion

- Malaysia – $399 billion

- Hong Kong – $381 billion

- Pakistan – $374 billion

1) 2024 Global Economy

- Global GDP – To increase to +3.2% in 2024, and +3.2% in 2025

- Global inflation – To decrease to +5.8% in 2024, and +4.3% in 2025

2) 2024 Global Outlook

- Global battle against inflation has largely been won

- Inflation peaked at 9.4% YOY in Q3 2022, projected to reach 3.5% by the end of 2025, below average level of 3.6% between 2000 and 2019.

- Global economy unusually resilient throughout the disinflationary process, avoiding a global recession.

- Downside risks are rising and now dominate the outlook: an escalation in regional conflicts, monetary policy remaining tight for too long, a possible resurgence of financial market volatility with adverse effects on sovereign debt markets, a deeper growth slowdown in China, and the continued ratcheting up of protectionist policies.

- World dominated by supply disruptions – from climate, health, and geopolitics.

- Harder for monetary policy to maintain price stability when faced with such shocks, which simultaneously increase prices and reduce output.

- Level of uncertainty surrounding the outlook is high – Newly elected governments (about half of the world population has gone or will go to the polls in 2024) could introduce significant shifts in trade and fiscal policy

- Little change in the global growth outlook since the April 2024 World Economic Outlook. Following the post-pandemic rebound, the global projection for GDP growth has been hovering at about 3%, both in the short and the medium term.

Assumptions:

- Commodity price assumptions – Oil prices are expected to rise by 0.9% in 2024 to about $81 a barrel

- Monetary policy assumptions – Compared with that in 2 April 2024, the anticipated trajectory of policy rates for major central banks in advanced economies has shifted. In the euro area, 100 basis points of cuts are expected in 2024 and 50 basis points in 2025, bringing the policy rate to 2.5 percent by June 2025. In the United States, the Federal Reserve pivoted to cutting rates in September, starting with a 50 basis point drop. The federal funds rate is projected to reach its long-term equilibrium of 2.9% in the third quarter of 2026, almost a year earlier than what was expected in April.

- Fiscal policy assumptions: Governments in advanced economies are on average expected to tighten their fiscal policy stances in both 2024 and 2025, halving primary deficits by 2029.

3) 2 Growth Upside

- Stronger recovery in investment in advanced economies

- Stronger momentum of structural reforms

4) 7 Downside Risks

- Monetary policy tightening

- Financial markets reprice as a result of monetary policy reassessments.

- Sovereign debt stress intensifies in emerging market and developing economies.

- China’s property sector contracts more deeply than expected.

- Renewed spikes in commodity prices arise as a result of climate shocks, regional conflicts, or broader geopolitical tensions

- Countries ratchet up protectionist policies

- Social unrest resumes

5) Central Bank policies recommendations / priorities:

- Carefully calibrate monetary policy.

- Mitigate disruptive foreign exchange volatility

- Restore macro-prudential buffers and ensure financial stability

- Urgently devise credible fiscal plans to avoid disruptive adjustments

- Safeguard growth-enhancing measures while reducing inequality

- Ensure debt sustainability.

- Advance macrostructural reforms

- Accelerate the green transition and address climate change

- Strengthen multilateral cooperation

6) IMF World Economic Outlook 2024 Forecast – October Update

For Investment Managers, Hedge Funds, Boutique Funds, Private Equity, Venture Capital, Professional Investors, Family Offices, Private Bankers & Advisors, sign up today. Subscribe to Caproasia and receive the latest news, data, insights & reports, events & programs daily at 2 pm.

Join Events & Find Services

Join Investments, Private Wealth, Family Office events in Hong Kong, Singapore, Asia-wide. Find hard-to-find $3 million to $300 million financial & investment services at The Financial Centre | TFC. Find financial, investment, private wealth, family office, real estate, luxury investments, citizenship, law firms & more. List hard-to-find financial & private wealth services.

Have a product launch? Promote a product or service? List your service at The Financial Centre | TFC. Join interviews & editorial and be featured on Caproasia.com or join Investments, Private Wealth, Family Office events. Contact us at angel@caproasia.com or mail@caproasia.com

Caproasia.com | The leading source of data, research, information & resource for financial professionals, investment managers, professional investors, family offices & advisors to institutions, billionaires, UHNWs & HNWs. Covering capital markets, investments and private wealth in Asia. How do you invest $3 million to $300 million? How do you manage $20 million to $3 billion of assets?

The 2025 Investment Day | 2025 Family Office Summits | Family Office Circle

2020 List of Private Banks in Hong Kong

2020 List of Private Banks in Singapore

2020 Top 10 Largest Family Office

2020 Top 10 Largest Multi-Family Offices

2020 Report: Hong Kong Private Banks & Asset Mgmt - $4.49 Trillion

2020 Report: Singapore Asset Mgmt - $3.48 Trillion AUM

For Investors | Professionals | Executives

Latest data, reports, insights, news, events & programs

Everyday at 2 pm

Direct to your inbox

Save 2 to 8 hours per week. Organised for success

Register Below

Get Ahead in 60 Seconds. Join 10,000 +

Save 2 to 8 hours weekly. Organised for Success.

Sign Up / Register

Please click on desktop.

Caproasia Users

- Manage $20 million to $3 billion of assets

- Invest $3 million to $300 million

- Advise institutions, billionaires, UHNWs & HNWs

Caproasia Platforms | 11,000 Investors & Advisors

- Caproasia.com

- Caproasia Access

- Caproasia Events

- The Financial Centre | Find Services

- Membership

- Family Office Circle

- Professional Investor Circle

- Investor Relations Network

Monthly Roundtable & Networking

Family Office Programs

The 2025 Investment Day

- March - Hong Kong

- March - Singapore

- July - Hong Kong

- July - Singapore

- Sept- Hong Kong

- Sept - Singapore

- Oct- Hong Kong

- Nov - Singapore

- Visit: The Investment Day | Register: Click here

Caproasia Summits

- The Institutional Investor Summit

- The Investment / Alternatives Summit

- The Private Wealth Summit

- The Family Office Summit

- The CEO & Entrepreneur Summit

- The Capital Markets Summit

- The ESG / Sustainable Investment Summit

Contact Us

For Enquiries, Membershipmail@caproasia.com, angel@caproasia.com

For Listing, Subscription

mail@caproasia.com, claire@caproasia.com

For Press Release, send to:

press@caproasia.com

For Events & Webinars

events@caproasia.com

For Media Kit, Advertising, Sponsorships, Partnerships

angel@caproasia.com

For Research, Data, Surveys, Reports

research@caproasia.com

For General Enquiries

mail@caproasia.com

a financial information technology co.

since 2014

& National Rally Party Convicted of €3 Million ($3.3 Million) Embezzlement with Marine Le Pe Sentenced to 4-Year Jail Term (2 Suspended + 2 Electronic Tag), €100,000 Fine & 5-Year Public Office Ban by France Court, Marine Le Pen & National Rally Party Diverted €3 Million from European Union (EU) Funds to Pay France Staff")

in Private Placement (Premium Price) via Shanghai Stock Exchange with Finance Ministry Investing $68.9 Billion (CNY 500 Billion), 4 Banks are Bank of China, Bank of Communications, China Construction Bank & Postal Savings Bank of China")

Collapsed in Thailand-Myanmar 7.7 Magnitude Earthquake on 28th March 2025, Building Construction is 30% Completed")

Announced to Buy 90% Interests in Panama Ports Company (2 Ports in Balboa & Cristobal) for $22.8 Billion in 2025 March")

, Glass & Aluminium")

Announces Organization Structure: Prominent Names Include ex-Indonesia Presidents Joko Widodo & Susilo Bambang Yudhoyono, ex-Thailand Prime Minister Thaksin Shinawatra, Hedge Fund Billionaire Bridgewater Associates Founder Ray Dalio, ex-Credit Suisse APAC CEO Helman Sitohang & Indonesia Minister of Finance Mulyani Indrawati")

Valuation with Existing Shareholder TPG Capital to Reinvest via TPG Asia Fund, Founded in 1997 by Alek Safarian Who Stepped Down as CEO in 2025 March")

& National Rally Party Convicted of €3 Million ($3.3 Million) Embezzlement with Marine Le Pe Sentenced to 4-Year Jail Term (2 Suspended + 2 Electronic Tag), €100,000 Fine & 5-Year Public Office Ban by France Court, Marine Le Pen & National Rally Party Diverted €3 Million from European Union (EU) Funds to Pay France Staff")

to Sell 33% of UBS Securities in China, UBS Currently Owns 67% of UBS Securities in China")

Succeeding Tan Sri Abdul Wahid Omar Who is Retiring (30/4/25) after 5-Year Tenure as Chairman, Tan Sri Abdul Farid Alias Has 30 Years of Financial Services & Banking Experience Including at Maybank, JP Morgan, Malaysian International Merchant Bankers & Schroders")